Financing a Granny Flat: Loans, Grants & Options

Building a granny flat is one of the more affordable ways to add space, boost property value, or create rental income. But even though it costs less than buying a new house, you still need a solid plan to pay for it.

The good news is there are several ways to finance a granny flat in Australia. You don’t always need to rely on one option. Many homeowners combine different methods depending on their situation.

This guide walks you through the most common financing options in simple terms, so you can decide what works best for you.

How Much Do You Need to Finance a Granny Flat?

Before looking at financing options, it helps to know how much you’ll likely need. Most granny flat projects in Australia sit between $120,000 and $200,000, depending on size, design, and site conditions.

Some builds can be cheaper if you go with a simple prefab design, while custom or high-end granny flats can go beyond $250,000. The exact number matters because it affects which financing option is realistic for you.

Using Home Equity (The Most Common Option)

For many homeowners, the easiest way to finance a granny flat is by using equity in their existing property.

What is home equity?

Equity is the difference between your property’s value and what you still owe on your mortgage. If your home has increased in value over time, you may be able to borrow against that value.

How it works

You can refinance your current home loan or take out a line of credit based on your equity. This gives you access to funds without needing to sell your property.

Why it’s popular

Using equity is often the preferred option because interest rates are usually lower than personal loans, and the repayment structure is more manageable. It also allows you to fund the granny flat without needing a large amount of cash upfront.

Construction Loans for Granny Flats

If you don’t want to refinance your existing loan, a construction loan is another option to consider.

How construction loans work

Instead of receiving all the money at once, the bank releases funds in stages as your granny flat is built. Payments are made at different milestones, such as slab, frame, and completion stages.

What to expect

During construction, you may only pay interest on the amount that has been used so far. Once the build is complete, the loan usually converts into a standard home loan.

When this option suits

This works well if you want a structured payment process and are building a custom granny flat rather than buying a simple prefab kit.

Personal Loans (For Smaller Builds)

A personal loan can be used to finance a granny flat, but it’s usually only suitable for smaller budgets.

Key things to know

Personal loans are faster to access and don’t require property as security. However, they often come with higher interest rates and shorter repayment terms compared to home loans.

When it makes sense

This option may work if your granny flat project is relatively low cost or if you only need to cover part of the total budget.

Using Savings or Cash

If you have enough savings, paying for your granny flat upfront can be the simplest option.

Benefits of using cash

You avoid interest payments and reduce financial stress over time. It also gives you more flexibility during the build process since you’re not tied to a lender’s requirements.

Things to consider

Using a large portion of your savings can reduce your financial buffer. It’s important to make sure you still have enough set aside for emergencies or unexpected costs.

Government Grants and Support

Depending on your location and situation, there may be government support available to help with building a granny flat.

Types of support that may apply

In Australia, direct grants specifically for granny flats are limited, but you may still benefit from broader housing or construction incentives. These can sometimes include support for first-home buyers, energy-efficient upgrades, or housing supply initiatives.

Important note

Grants and eligibility rules can change over time and vary by state, so it’s always worth checking with your local council or state government website for the latest information.

Family Support or Shared Investment

Another option that is becoming more common is financing a granny flat with help from family members.

How this works

Family members may contribute funds in exchange for living in the granny flat or sharing rental income. In some cases, it’s used as a way to support aging parents while keeping living arrangements close and practical.

What to keep in mind

It’s important to have clear agreements in place, even if it’s within family. This helps avoid misunderstandings later on.

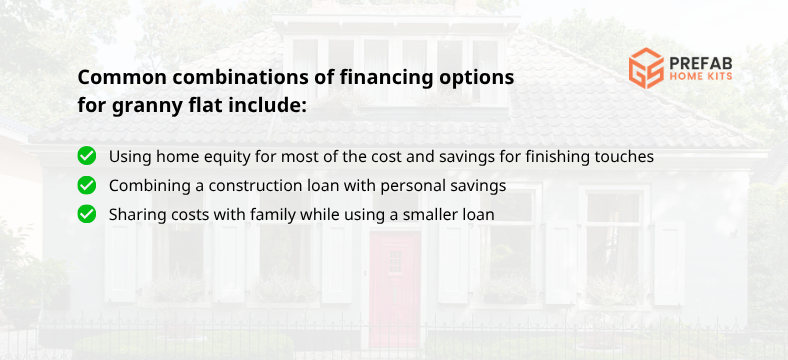

Combining Financing Options for Granny Flat

You don’t have to choose just one method. Many homeowners use a mix of options to finance their granny flat. This flexible approach can reduce financial pressure and make the project more achievable.

Things to Consider Before Choosing a Financing Option for a Granny Flat

Before deciding how to finance your granny flat, it’s important to look at the bigger picture.

Your repayment ability

Make sure you can comfortably manage repayments if you take out a loan. It’s better to plan conservatively rather than stretch your budget too far.

Your long-term goals

Think about why you’re building the granny flat. If it’s for rental income, you can factor in future earnings. If it’s for family use, the financial return may be less important than lifestyle benefits.

Interest rates and loan terms

Different financing options come with different interest rates and conditions. Even a small difference in rate can have a big impact over time.

Can a Granny Flat Pay for Itself?

One of the reasons many people choose to build a granny flat is the potential for rental income.

In many parts of Australia, a granny flat can generate between $250 and $600 per week, depending on location and quality. Over time, this income can help cover loan repayments and reduce the overall cost of the investment.

While it may not fully pay for itself immediately, it can significantly ease the financial burden.

Common Mistakes to Avoid

When financing a granny flat, a few common mistakes can lead to unnecessary stress.

Underestimating total cost

Many people focus only on construction costs and forget about approvals, site preparation, and finishing touches.

Not allowing a buffer

Unexpected costs can come up during the build. Having a financial buffer of around 10–15% can help you stay on track.

Choosing the wrong loan type

Not all loans are suited for granny flat projects. Taking time to compare options can save you money in the long run.

Final Thoughts

Financing a granny flat doesn’t have to be complicated. With the right approach, it can be a manageable and worthwhile investment.

Whether you use home equity, a construction loan, savings, or a combination of options, the key is to choose a solution that fits your financial situation and long-term goals.

A well-planned granny flat can provide extra space, support family living, and even generate income. With the right financing strategy, it becomes not just an expense, but a smart addition to your property.

Get a FREE quote for a granny flat here.

Explore more ideas at our Prefab Home Kits Fanpage.